Gold prices at all-time highs

Gold prices extended their record-breaking rally this week, surpassing $4,100 per ounce amid a surge in safe-haven demand. Political uncertainty in the United States including the ongoing government shutdown, the absence of a clear reopening timeline, and growing concerns over its economic impact has boosted demand for gold.

Adding to the momentum, renewed U.S.-China trade tensions have resurfaced after President Trump threatened to impose 100% tariffs on Chinese imports, though he later softened his stance. Meanwhile, mounting worries over Federal Reserve independence and a weaker U.S. dollar, as markets price in multiple rate cuts have further fueled the rally.

Gold also continues to benefit from strong central bank demand, a key structural driver of its long-term strength. Looking ahead, the direction of U.S. inflation will play a critical role in shaping gold’s next move. Persistently high inflation could push real interest rates (nominal rates minus inflation) lower, supporting further gains in gold. Conversely, if inflation eases, risk appetite may recover, putting downward pressure on prices.

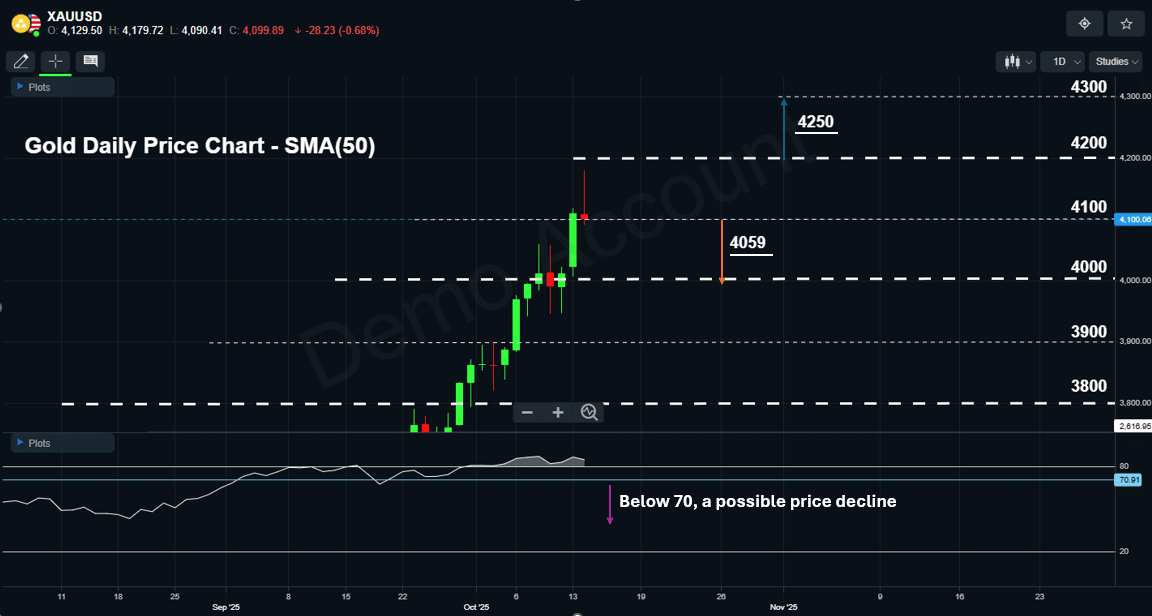

Gold – Technical Outlook

Last week, gold decisively broke above the $4,000 per ounce barrier and continued higher into the $4,100–$4,200 trading zone. Prices now appear poised to test the high end of this zone. A daily close above $4,200 would confirm continued buying momentum, potentially opening the path toward $4,300. However, the resistance level of $4,250 should be closely monitored.

Levels to Watch in a Pullback Scenario

A daily close below $4,100 would suggest fading bullish momentum due to profit-taking, possibly triggering a deeper correction toward $4,000. A daily close below that level could expose the market to further downside toward $3,900.

The Relative Strength Index (RSI) remains in overbought territory; a drop below 70 would signal a loss of upward momentum and increase the likelihood of a pullback.